Maximizing Owner-Only Opportunities

A JULY owner-only solution can help you optimize retirement savings and tax benefits

JULY specializes in helping owner-only businesses maximize retirement savings. We’ll work with you and your advisor or CPA to design a plan that provides much greater flexibility and savings potential than is available through a SEP or SIMPLE plan.

SOLOK 401(k) Plans

A SOLO 401(k) Plan allows contributions up to $72,000 ($80,000 if age 50) and provides access to funds via tax-free loans and early withdrawal features.

$30

monthly plan fee

$30

per participant

Add a SOLO Cash Balance Plan

Cash Balance Plans are designed for those seeking to fund much larger contributions than is permitted in 401(k) plans, SEPs, and SIMPLEs. Contributions: $150,000 or more.

$167

monthly plan fee

$250

per participant

What You Can Expect

We work with you and your advisor or CPA to create a good fit.

We make it easy for you to start a plan.

We handle contribution calculations, recordkeeping, compliance, and reporting.

We work with you and your advisor to keep you on track for success.

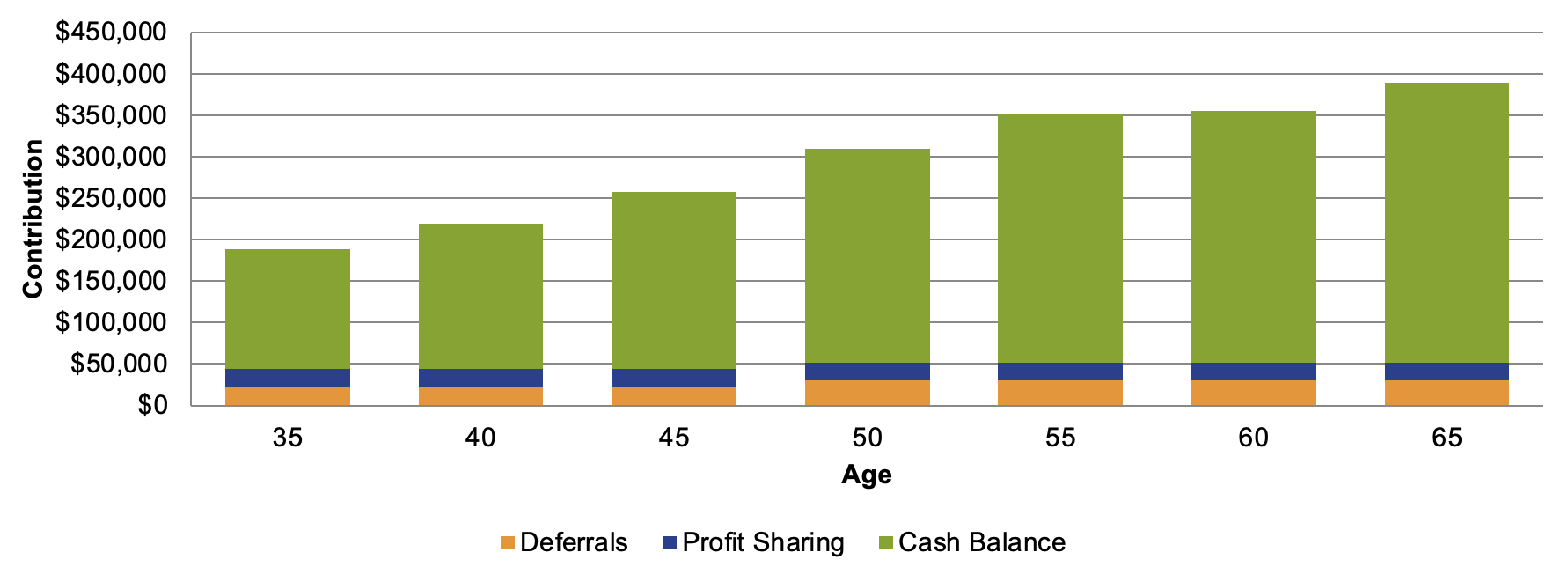

Look at the Contribution Potential of a

401(k) + Profit Sharing + Cash Balance

Is a Cash Balance Plan a Good Fit?

Cash Balance plans are well-suited for most sole proprietors, partnerships, and partnerships with multiple partners. Spouses that work in the business can participate, too.

Annual Contributions Are Required

Contributions to Cash Balance Plans must be made annually. In some circumstances, the plan can be amended to lower contributions, but strict IRS regulations may require the plan to remain in place for up to 10 years.

Steady Cash Flow is Important

Annual contributions are based on owners’ annual compensation or earned income. Because contributions are required, steady cash flow is needed to ensure the plan can be funded each year.

Contributions May Fluctuate

Cash Balance Plans are a type of Defined Benefit Plan and fund to a target retirement benefit. Contributions can vary from year to year based on investment earnings, interest rates, and other actuarial factors.

It’s easy to get started!

We ask a few questions to understand your company and goals.

We match you to a plan that fits you now and that can grow with you.